Sector outlook

Passenger traffic expected to see further growth in financial year 2026

The International Air Transport Association (IATA) predicts that global passenger traffic – measured by global revenue passenger-kilometres – will grow year-on-year by 5% in 2026 (previous year: 5%) despite geopolitical crises and significant delivery bottlenecks for new aircraft.

The fastest growth of 7% is expected for the Asia/Pacific and Latin America regions, followed by the Middle East and Africa, both at 6%. Growth of 4% is predicted for Europe and 2% for North America.

Financial analysts are anticipating robust demand for European airlines in 2026, driven in long-haul traffic by ongoing strong premium leisure travel. In inner-European traffic, however, the assumption is that strong competition among airlines will cause fares to be more stable year-on-year. Overall, it seems that consumers’ willingness to spend on travel will also remain remarkably high. Demand for travel should therefore perform better than the general state of the European economy would currently suggest.

In addition to solid developments in demand, the assumption is that supply will remain limited – for example, due to a lack of staff at airports, in air traffic control and at airlines, as well as delays in the delivery of new aircraft. Capacity growth will therefore again be limited by external factors, and is expected to be similarly moderate in 2026 as in the previous year. Even if the faults affecting the Pratt & Whitney GTF engine family are largely overcome, inner-European traffic will not grow to the same extent as intercontinental traffic, where capacity is expected to expand by at least 5%. Yields for European airlines in the North Atlantic region will likely only increase slightly due to the currently weak US dollar and ongoing political volatility, even though capacity is severely reduced at present. For South Atlantic traffic, by contrast, capital markets are expecting the demand boom to continue and customers’ willingness to pay to remain strong.

The picture has increasingly stabilised in Asia and particularly in China in recent years. Macroeconomic challenges and capacity growth far above the sector average have caused European airlines to cut their capacities accordingly and focus on the most profitable routes. By contrast, other regions in Asia, such as India, Thailand and Japan, are playing an increasingly important role for European airlines.

In terms of yields in the passenger business, IATA is expecting a year-on-year decline of 0.1% in 2026 (previous year: decline of 0.9%).

Airfreight set to increase again in 2026

As in the previous year, IATA forecasts around 3% growth in revenue cargo tonne-kilometres in 2026 for global airfreight traffic (previous year: growth of 3%).

Yields in the cargo business are again forecast to decline slightly by 0.5% in 2026 (previous year: decline of 0.5%).

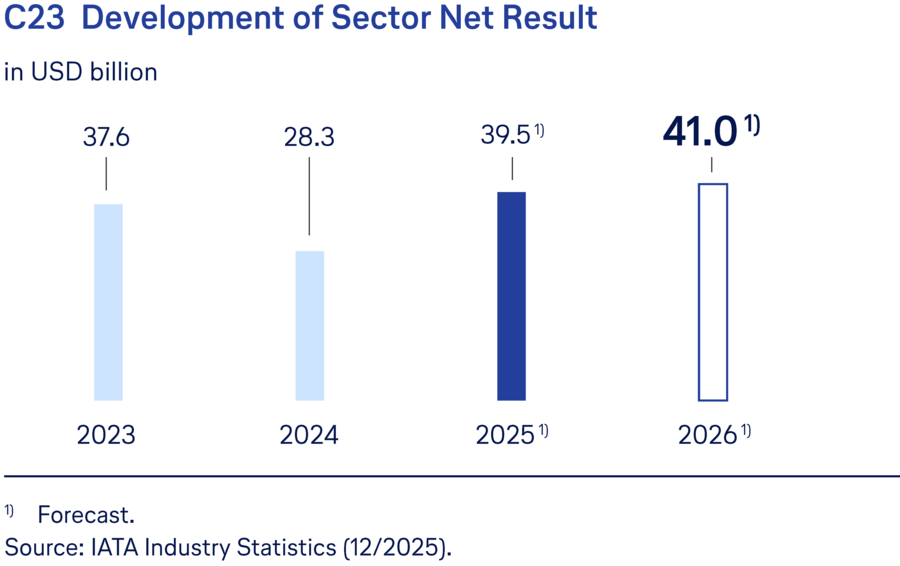

Net profit of USD 41bn forecast for the industry

The industry is expected to report a net profit of USD 41.0bn (previous year: USD 39.5bn).

Further growth expected in MRO market

The aviation industry is in a period of transition from conventional aircraft models to new, more efficient technologies. However, supply chain problems are preventing the leading aircraft manufacturers from reaching their original plans for production rates. This affects both the major aircraft manufacturers, Boeing and Airbus, equally.

The new engine technologies, such as the Pratt & Whitney GTF engine family and the LEAP engine family from CFM International, also have to be retrofitted with upgrades and modifications at the request of the authorities. The consequence is that these next-generation engines have to be integrated into the still-developing repair networks earlier than originally anticipated. At the same time, demand remains high for maintenance services for legacy-generation engine models, because the airlines are obliged to use them for longer. Demand for maintenance and repair services is also growing due to the ongoing strong demand for air travel.

The consultancy firm ICF predicts average growth for the MRO market (not including embargoed countries) of 6% in 2026 compared with the previous year. Growth rates in the individual regions are forecast to be 11% for the Americas, 7% for Asia/Pacific and 2% for Europe, Middle East and Africa. However, this growth can still be affected significantly by external influences such as geopolitical factors, tariffs, inflation or supply chain instability.